Everybody Talks Revolut's AI. Nobody Talks Insurance.

Everybody is talking about Revolut's new AI. Almost nobody is talking about what it means for insurance. That needs to change.

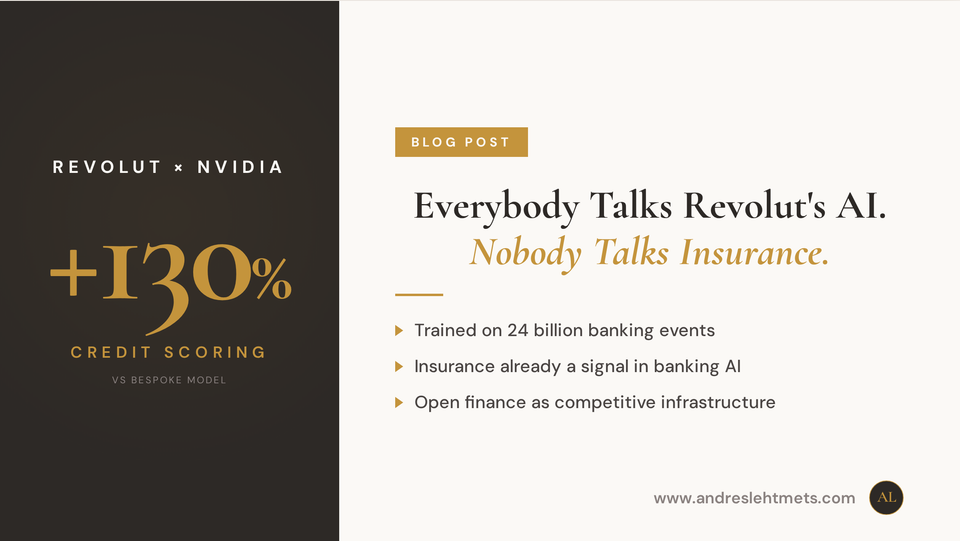

Revolut, together with NVIDIA, recently published a paper introducing PRAGMA, a "foundation model for banking." It is worth unpacking that phrase, because it is doing a lot of work.

A foundation model is trained once, on an enormous dataset, to learn general patterns. It is then adapted to many specific tasks without being retrained from scratch. ChatGPT is a foundation model for language. PRAGMA is the same idea, applied to customer behaviour inside a bank.

This is not another LLM take. PRAGMA does not read, write, or chat. It learns directly from the structure of financial events, because text tokenisation breaks the signal in financial data. Dollar amounts fragmented into digits lose their meaning. This is a different kind of model, built for a different purpose.

Revolut trained it on 24 billion events from 26 million customers across 111 countries, over 25 months. Transactions, card usage, app interactions, communications, trading behaviour, all folded into one learned representation of the customer.

Then they tested it on six of their own internal tasks, the kind of predictions every bank runs every day. The results are notable, especially given they are benchmarked against Revolut's own production models:

- Credit scoring: +130% vs Revolut's existing bespoke model

- External fraud detection: +65%

- Marketing engagement prediction: +79%

- Product recommendation: +40%

These are not absolute accuracy figures. They are improvements over models that were already purpose-built for their specific tasks. One general-purpose model now beats a whole suite of specialised ones, at least in Revolut's own setup, on their own data. For a bank, that is a structural change in how AI gets built.

Now the part I find most interesting.

Among the profile attributes the model learns from, the authors include one word: "insurance state." It is a small, almost incidental signal, but a telling one. Insurance is already being folded into a broader financial behaviour model, as one more feature in the unified picture super-apps are quietly assembling.

Meanwhile, most insurers are still building AI in silos. Claims data. Underwriting. A narrow slice of the customer's life.

This is not a race about who has the better model. It is a race about who has the better unified view of the customer.

If your competitor can see your customer's spending, savings, credit, fraud risk, and insurance state, while you only see their insurance history, model quality becomes secondary to data scope.

This, for me, is the quiet case for open insurance and FIDA. Not as a compliance burden. As the infrastructure that lets insurers build comparable behavioural capabilities, without needing to be a super-app first.

The question insurers should take from the PRAGMA paper is not "how do we build our own."

It is "what access to data do we need to compete with institutions that already have one."

I write about this kind of shift every week in my newsletter.

Member discussion